What Is Delisting of Shares?

Delisting of shares The term delisting of shares is used to refer to a permanent withdrawal of the securities of a company on a recognized stock exchange, essentially transforming the company into a privately owned company. This procedure removes the capability of the investors to sell or purchase shares in the formal exchange platform which has a great influence on liquidity and price discovery procedures. Delisting in India is regulated by section 21A of the Securities Contracts (Regulation) Act, 1956 and in-depth regulations by the Securities and Exchange Board of India (SEBI).

The delisting procedure radically changes the relationship of a company with the public markets and regulatory control. After delisting, companies are no longer obligated to abide by the continuous disclosure, quarterly reporting and high corporate governance standards that are mandatory to listed companies. But they have to keep complying with provisions of Companies Act, 2013 and with minimum regulatory compliance with the Registrar of Companies.

To investors, delisting is a critical point that impacts on their liquidity in investment, valuation processes and exit strategies. The shares become illiquid, and shareholders have to depend on either private trading, over-the-counter markets, or buy back of the company to sell the shares. The delisting implications are important to understand in order to make a sound investment decision.

Types of Delisting of Shares

Voluntary Delisting

Voluntary delisting is a situation, which is initiated by the management and controlling stockholders of a company that want to voluntarily withdraw shares in stock exchanges. This is usually a strategic move based on the need to restructure the business, cost cutting measures or the need to have flexibility of operation without the pressure of a public market. It must be approved by special resolutions by the shareholders, and the majority of the votes cast were in favor of the proposal, which is 75 percent or more.

Companies can therefore voluntarily delist in two different ways, under new amendments to the Reverse Book Building (RBB) process that have been introduced by SEBI under the new amendments that came into effect on September 25, 2024, namely in the Fixed Price mechanism. The Fixed Price option enables firms that have actively traded shares to open a specified price that will need to be at least 15 percent higher than the computed floor price, which will give them more assurance and less speculative bidding problems, as experienced during previous delisting efforts

Compulsory Delisting

Stock exchanges or SEBI impose compulsory delisting to companies which do not meet the listing requirements or regulatory standards which are stipulated. Some of the common triggers are the persistent failure to adhere to disclosure norms, minimum shareholding quota, inability to submit compulsory financial reporting or extended trading suspension as a result of a variety of violations. The first step is the suspension phase of not less than six months, during which companies are allowed to correct their compliance problems.

Before a company is forced out of business through a compulsory delisting process, stock exchanges should give it sufficient time to rectify shortcomings. The ruling must have reasons written down and in accordance with certain schedules and exchanges trying to fulfil a prescription of nine months when the ruling is initiated. This process safeguards market integrity as it eliminates non-compliant parties and it provides procedural fairness.

Reasons Why Companies Opt for Delisting

Cost Optimization and Regulatory Relief

A significant amount of continuous cost is incurred by listed companies in the form of annual listing fees, compliance costs, audit cost, and regulatory violation penalties. These are cumulative costs that have a big effect on profitability especially to small firms or those operating in poor business cycles. Delisting gets rid of these repeated financial liabilities and has a side effect of simplifying the administrative aspects of ongoing regulatory compliance.

Ownership Consolidation and Strategic Flexibility

Delisting is usually sought after by promoters and controlling shareholders to have full ownership of the company without restrictions by the minority shareholders. Through this consolidation, it is possible to make decisions more quickly, create changes in strategies and reorganization efforts that could be opposed in open discussion. There are also simpler mergers, acquisitions or transformation of business models using private ownership structures without long shareholder approvals and regulatory requirements.

Market Performance and Liquidity Concerns

Public listing may not be conducive to companies whose daily and overall trading volumes are low, market performance poor or whose institutional interest is limited. A negative market reception may lead to a negative perception cycle, which may impact on the business relationship and employee morale. Delisting also enables such companies to continue their business without the direct attention of the market whilst they concentrate on the underlying business enhancements.

Restructuring and Financial Engineering

Delisting may be required to facilitate a complex change of ownership, such as in the case of a corporate restructuring, such as a leveraged buyout or family succession planning, or a private equity transaction. The undertakings of these strategies usually demand flexibility and secrecy in operations which cannot easily be achieved in the open market.

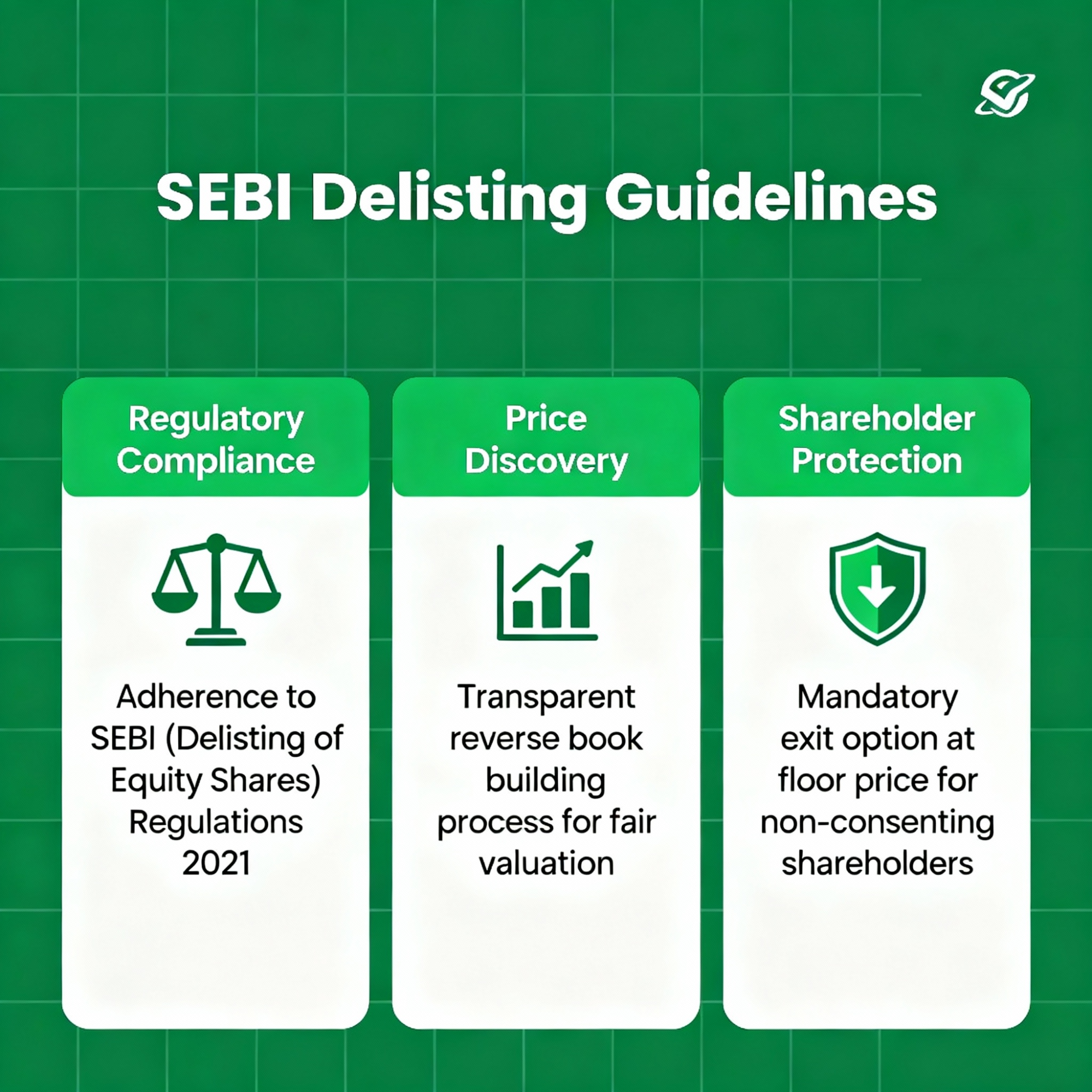

SEBI Guidelines on Delisting of Shares

SEBI's comprehensive regulatory framework, embodied in the Securities and Exchange Board of India (Delisting of Equity Shares) Regulations, 2021, establishes detailed procedures ensuring investor protection while facilitating legitimate business needs. Recent amendments effective September 2024 introduced significant flexibility while maintaining robust safeguards for minority shareholders.

Price Discovery and Floor Price Determination

Under the amended regulations, floor price calculation incorporates multiple parameters to ensure fair valuation: volume weighted average price (VWAP) for acquisitions over preceding 52 weeks, highest acquisition price during 26 weeks prior to reference date, market VWAP for 60 trading days before announcement, and newly introduced "Adjusted Book Value" determined by independent registered valuers considering consolidated financial statements.

Fixed Price Delisting Framework

The revolutionary Fixed Price mechanism allows companies with frequently traded shares to offer predetermined delisting prices, providing certainty for both promoters and shareholders. The minimum offering must exceed floor price by at least 15%, reducing speculative bidding and artificial price inflation that characterized earlier RBB processes. This mechanism streamlines delisting while ensuring fair exit opportunities.

Investment Holding Company (IHC) Special Provisions

SEBI introduced specialized delisting frameworks for Investment Holding Companies where at least 75% of fair value comprises direct investments in other listed companies. These entities can utilize court-approved schemes involving pro-rata distribution of listed securities to public shareholders, cash payments for unlisted investments, and selective capital reduction mechanisms, providing tailored solutions for complex holding structures.

Minority Shareholder Protection

Comprehensive exit opportunities ensure minority shareholders receive fair treatment through mandatory buyback offers at determined prices. Counter-offer thresholds were reduced from 90% to 75% shareholding acquisition, provided at least 50% of public shareholding participates, making successful delisting more achievable while maintaining protective mechanisms.

Step-by-Step Process of Delisting in India

Phase 1: Preliminary approvals and Publicity

Delisting process starts with board resolutions previously endorsing delisting proposals and then the appointment of SEBI registered merchant bankers as managers of the process. The firms should announce in the market their plans to delist, the reasons behind it, and the timeframes and the methods of exit. This transparency stage will give proper information to all the stakeholders to make informed decisions.

Phase 2: Special Resolution of Shareholders

Voluntary delisting takes special resolutions of at least 75 percent of votes cast by postal ballot or e-voting systems. The independence of the voting of shareholders can be a separate issue in order to avoid promoter interests dominating over the minority interest. This is a democratic process, which makes major corporate decisions to be widely agreed upon by stakeholders.

Phase 3: Discovery Phase of the price

Firms that opt to use RBB perform reverse book building whereby shareholders place price bids as to their willingness to sell. Alternative Fixed Price routes are routes where predetermined prices above floor calculations are offered with a minimum 15 percent difference. Price discovery that creates a right valuation based on true market feeling as opposed to arbitrary determination.

Phase 4: Exit Offer and Share Tendering

Effective price discovery, in turn, results in formal exit proposals and in the process whereby, in the course of the process, the shareholders of the companies that are publicly traded can offer to sell their shares at considered prices within a given time frame. Tendered shares have to be bought by a promoter or acquiring entity who will ensure the exit of the investors by giving them certain liquidity. This is a mechanism that helps minority shareholders to avoid being stuck in liquidity investments.

Phase 5: Regulatory Approvals and Final Delisting

The applications presented to the stock exchanges are regulated to ensure that they meet all the requirements in the procedures, fair pricing and sufficient protection of minorities. When all the terms have been met successfully, the exchanges take shares off trading platforms. After delisting, businesses remain compliant with statutory requirements under Companies Act and do not have to comply with any exchange-related requirements.

Impact of Delisting on Shareholders

Liquidity Constrained and Constrained Exits

The immediate effect is the total absence of liquidity in the secondary market where the shares will stop trading in the organized markets. The shareholders are not able to conduct immediate buy-sell transactions and this can hold up capitals. There is a reduced flexibility in portfolios as the only exit options are the use of private negotiations, over-the-counter, or future corporate moves.

Valuation and Price Discovery Problems

In the absence of continuous market trading the correct price discovery is difficult since the shares do not have real-time valuation mechanisms. The fair value of shares has to be based on periodic independent valuation, negotiated transaction prices, or company-provided buyback offers by shareholders. This opaceness may cause conflicts about coping with the compensation in the case of an exit.

Asymmetry of information and Decreased Transparency

Delisted corporations do not attract much disclosure as listed corporations, which poses a tremendous information vacuum to investors. The shareholders no longer have access to quarterly financial reports, frequent corporate news releases, and unbiased research coverage, and making informed investment decisions are even more challenging. This imbalance is more disadvantageous especially to the retail investors who are not in direct access to the company.

Minority Shareholder Rights and Governance Concerns

The increased ex-post control of promoters by delisting can affect the quality of governance and protection of minority shareholders. In the absence of market regulation and control by society, decision making can be less transparent. Nonetheless, the SEBI laws require equitable exit deals and pricing measures to maintain the interests of the minorities in the delisting process.

Taxation and Capital Treatment

The capital gains taxation can be caused by the holding periods and the structure of the transactions made by the sale of shares during the delisting or subsequent private sale. Long-term investments are usually given the preferential taxation whereas short-term transactions are taxed at higher rates. In determining whether to exit in a delisting offer or to hold on to the shares in the event of future opportunities, the shareholders should consider tax implications of the share.

Conclusion

Delisting shares in India is a major corporate move that is subject to elaborate regulations by SEBI that aim to create the right balance between acceptable business flexibility and effective investor protection. Recent changes in the regulatory frameworks with the introduction of Fixed Price systems and Investment Holding Company models show the desire of SEBI to respond to some of the practical challenges but still ensure the integrity of the market. Delisting becomes less complex due to these developments and makes companies with operational flexibility more likely to be treated fairly to shareholders in the public.

To investors the implication of delisting is very important to make informed decisions of their portfolio and to safeguard the interests of their investments. Although delisting potentially presents benefits such as buyback premiums and strategic flexibility to the companies, it essentially changes elements of investment liquidity, and risk profiles. During delisting shareholders should be cautious of exit opportunities in delisting processes because of the long-term effects of holding illiquid securities.

The regulatory environment is changing in line with international best practice, but to meet the market conditions and investor protection requirements in India. A well-established delisting structure adds to the overall efficiency of the capital markets as they offer a feasible exit status to firms whilst still conforming to their faith in the public market system. The only way to achieve success is to remain vigilant with regard to regulations, transparent processes and balanced attention to all stakeholder interests during the delisting journey.