SEBI Delisting Regulations Explained for Investors

30 June 2025

17 min read

When a company's shares disappear from the stock exchange, it's called delisting. For investors, this means the familiar process of buying and selling those shares on the open market comes to a halt. Getting to grips with the why and how of this process is the first critical step in understanding SEBI delisting regulations and protecting your investment.

Why Companies Leave the Stock Market

Think of a bustling public market where anyone can set up a stall. Delisting is like one of the most prominent stall owners deciding to pack up and turn their business into an exclusive, invitation-only boutique. A publicly-traded company essentially does the same thing—it chooses to remove its shares from the stock exchange, transitioning from being publicly owned to privately held.

So, why would a successful company make this move? The reasons are almost always strategic and financial. Staying listed comes with a heavy price tag and a lot of work. There are quarterly financial reports, mountains of compliance paperwork, and the constant glare of public scrutiny. Going private allows a company’s management to focus on long-term strategy without the relentless pressure of hitting quarterly targets for the market.

Key Drivers Behind Delisting

A few other common reasons often push a company to delist:

Operational Flexibility: As a private entity, a company can make big decisions much faster. There's no need to go through lengthy shareholder approval processes for every major initiative.

Shedding the Compliance Burden: Delisting cuts out the significant costs and administrative headaches tied to stock exchange listing agreements and SEBI's demanding disclosure norms.

Corporate Restructuring: Often, delisting is just one piece of a much larger puzzle. It could be part of a merger with another company, a strategic acquisition, or a complete business overhaul.

Low Trading Volume: If a company's shares are rarely traded, the benefits of being on a public exchange just don't justify the costs anymore. Delisting becomes a practical financial decision.

The Two Paths to Delisting

A company can exit the stock market in one of two ways. Each path has vastly different implications for you as an investor.

1. Voluntary Delisting: This is when the company's promoters or key shareholders decide to take the company private. They kick off the process by making a formal offer to buy back all the shares held by the public. This is the "exclusive boutique" scenario we talked about—a deliberate choice made by the company. The entire process is strictly overseen by SEBI delisting regulations to make sure minority shareholders get a fair price and a proper exit.

2. Compulsory Delisting: This is the opposite. It's a penalty imposed by the stock exchange or SEBI itself. It usually happens when a company consistently breaks the rules of the listing agreement—things like not paying annual fees or failing to file financial statements on time. The company is essentially kicked off the exchange. Although the promoters are still legally required to offer an exit opportunity to public shareholders, this is a major red flag about the company’s governance and financial stability.

To give you a clearer picture, let's break down the core differences.

Voluntary vs Compulsory Delisting at a Glance

This table offers a quick comparison to help you distinguish between the two types of delisting at a glance.

Aspect

Voluntary Delisting

Compulsory Delisting

Initiator

The company's promoters or acquirers.

The stock exchange or SEBI as a penalty.

Reason

A strategic business decision (e.g., restructuring, going private).

Non-compliance with listing agreements or regulations.

Investor Perception

Generally neutral or positive, seen as a corporate action.

Highly negative, viewed as a sign of poor governance or financial trouble.

Exit Price

Determined through a Reverse Book Building process to discover a fair price.

Determined by an independent valuer appointed by the exchange.

Process

A structured process initiated by the company with shareholder approval.

A punitive action taken against the company.

Understanding this distinction is crucial. A voluntary delisting is a planned corporate event, whereas a compulsory one is a regulatory slap on the wrist. If you find yourself holding shares in a company that's been delisted, knowing your next steps is vital. You can find more detailed guidance on what to do in our article on how to sell delisted shares. With this foundation, you're ready for a deeper dive into the specific rules that protect your interests.

The Evolution of Delisting Rules in India

To really get to grips with today’s SEBI delisting regulations, you have to understand where they came from. These rules weren't just created out of thin air. They've been shaped and reshaped over decades, adapting as the Indian market became more intricate and mature. This whole journey is a story of SEBI’s continuous effort to find that sweet spot—giving companies the flexibility they need while fiercely protecting the everyday investor.

At its heart, the evolution of delisting regulations is about strengthening investor protection. The early rules were fairly basic. But as the market grew up, it became obvious that a more structured and transparent process was needed. SEBI saw the risk: if promoters could take a company private without strong checks and balances, minority shareholders could easily be left holding the short end of the stick with a lowball offer.

This realisation kickstarted a series of crucial updates designed to even the odds. The guiding principle has always been to ensure that when public shareholders are asked to sell their shares back, the entire process is fair, transparent, and gives them a real say in the matter.

The Early Framework and Key Turning Points

The first set of rules for delisting shares in India looks nothing like what we have today. A landmark circular from April 29, 1998, was a huge leap forward. It brought in a structured framework that required shareholder approval through a special resolution. More importantly, it set a minimum exit price, pegging it to the weighted average price of the stock over the previous six months. You can even explore the original SEBI circular to see these foundational ideas.

This was a game-changer. For the first time, promoters couldn't just pull a price out of a hat. A floor was established, creating a much-needed safety net for investors. It was a clear signal that the regulator was shifting power back towards a more balanced, controlled environment.

From this foundation, the rules kept developing. The introduction of the Reverse Book Building (RBB) process in 2003 was another pivotal moment. The idea was to let the market itself—through shareholder consensus—discover the true exit price.

From the 2009 Rules to the 2021 Regulations

For over a decade, the SEBI (Delisting of Securities) Guidelines, 2009, served as the main rulebook, pulling together and refining all the previous directives. But the market never stands still. New challenges, like concerns over price manipulation and the sometimes clunky RBB process, showed that there was still room for improvement.

This led SEBI to conduct a thorough review, resulting in the current SEBI (Delisting of Equity Shares) Regulations, 2021. These weren’t a complete rewrite but a significant fine-tuning of the existing framework. The goal was to make the delisting process more efficient while doubling down on the safeguards for minority shareholders. Key changes focused on timelines, counter-offer mechanisms, and the responsibilities of promoters, making the entire system much more solid.

This historical backdrop is crucial because it explains the why behind today's rules. Every single requirement, from how the floor price is calculated to the 90% shareholding threshold, exists because of lessons learned from the past. It’s a journey that also provides useful context for those tracking a company from private to public, a process we detail in our guide to the IPO process. It all highlights SEBI's long-standing commitment to building a market where both promoters and public shareholders can act with confidence.

A Practical Guide to SEBI's Delisting Framework

Taking a company private isn't as simple as flicking a switch. It's a complex journey from being a publicly traded entity to a private one, meticulously guided by SEBI to protect everyone involved, especially the public shareholders. This whole process is defined by the SEBI delisting regulations, which act as a detailed playbook for companies and a crucial safety net for investors.

Before a company's promoter can even think about buying out public shareholders, the company has to clear some basic hurdles. Think of these as the entry ticket to the delisting process. For starters, the company’s shares must have been listed on a recognised stock exchange for at least three years. On top of that, the company needs a clean record, with no major violations of securities laws during that time.

These initial checks are there for a reason. They ensure that only established, well-behaved companies can start a voluntary delisting, preventing dodgy operators from using it as a back-door exit.

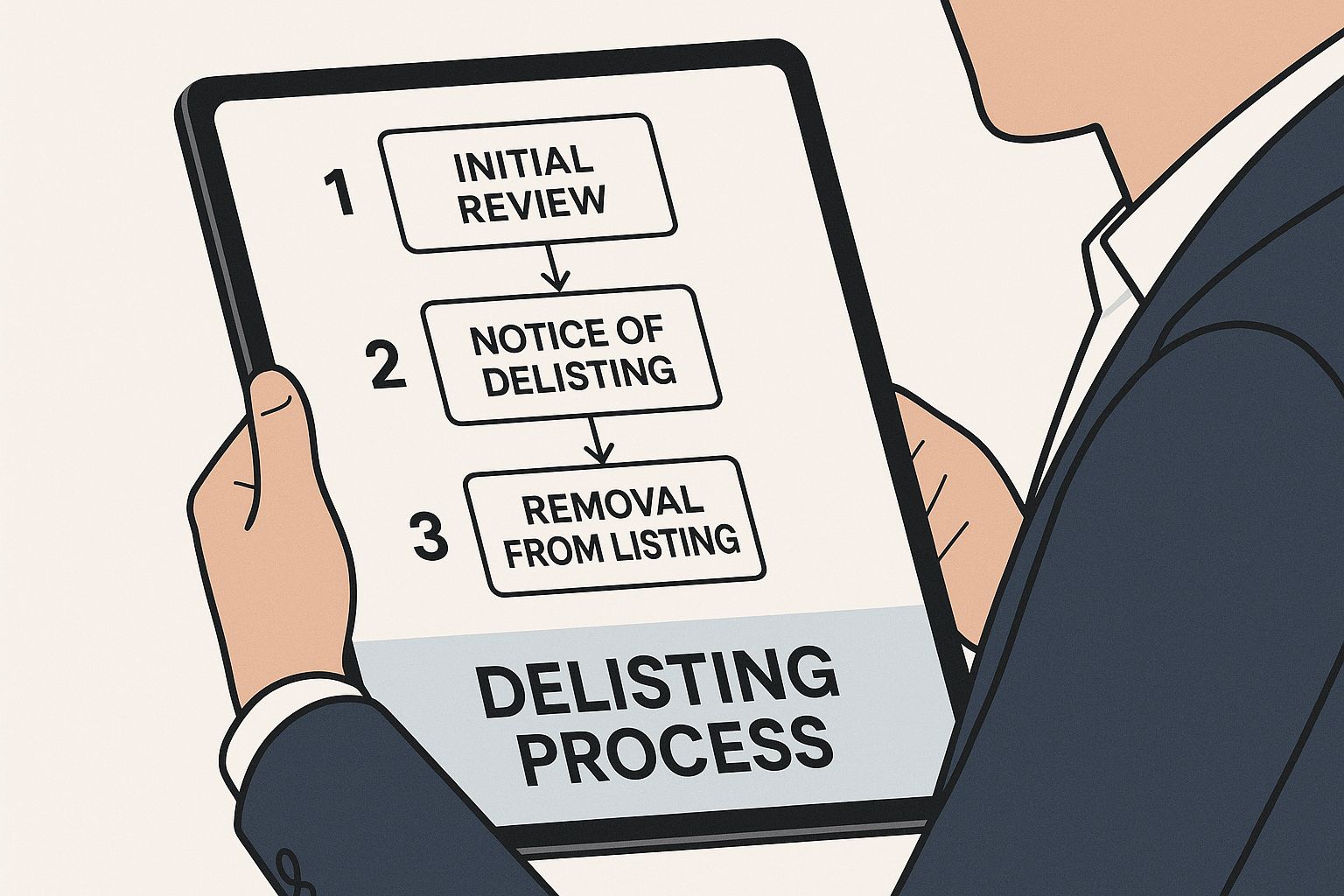

The infographic below gives you a bird's-eye view of how the delisting process unfolds, from the initial proposal to the final exit.

As you can see, it's not a single event but a series of carefully planned steps involving multiple approvals and public announcements.

The Step-by-Step Delisting Procedure

Once a company passes the eligibility test, a strict timeline of events kicks in, all defined by SEBI to keep the process orderly and fair.

It all starts with a board meeting. The company's directors must approve the delisting proposal, and they can't just rubber-stamp it; they need to provide solid reasons for the decision. Right after, this news goes public through announcements to the stock exchanges and in newspapers, making sure every single investor knows what’s happening.

Next up is a crucial democratic checkpoint: shareholder approval. The company has to get a special resolution passed by its shareholders. This is where minority shareholders really get to have their say.

This "two-to-one" rule essentially gives minority shareholders a powerful veto, a standout feature of the SEBI delisting regulations.

Key Players and Investor Safeguards

SEBI has built several checks and balances into the system by requiring independent experts to oversee the process. First, the company must appoint a merchant banker, who essentially manages the delisting offer. Their role is to ensure everything is done by the book, from regulatory compliance to acting as the go-between for the company, its shareholders, and the stock exchange.

The company's independent directors also have a vital part to play. They are required to give a reasoned, unbiased recommendation on the delisting proposal, looking out for the interests of all shareholders, particularly the public minority. This provides another layer of independent review.

The current rules, the SEBI (Delisting of Equity Shares) Regulations, 2021, were a significant update to the older 2009 framework. They were brought in to make the process more efficient while strengthening protections for minority investors. You can discover more about the 2021 delisting rule changes to understand their full market impact.

So what happens after delisting? The shares don't just disappear. They simply move from the public stock market to the private one. For those curious about this world, our guide on unlisted shares in India is a great starting point. This robust regulatory structure is precisely what makes India’s delisting process one of the most well-regarded in the world.

How Is the Delisting Price Figured Out?

When a company announces it’s going private, the first question on every shareholder's mind is always the same: "So, what's my exit price?" This isn't just a number the company’s promoters can dream up. The SEBI delisting regulations lay out very clear and structured ways to arrive at this price, making sure the whole affair is transparent.

First things first, the promoter can't just lowball everyone. They have to start by calculating a floor price—this is the absolute minimum they're legally allowed to offer. Think of it as a safety net for shareholders. This price is worked out using a specific SEBI formula that looks at the stock's recent trading history to set a fair starting point. But the final price shareholders receive is often much higher, determined by one of two very different paths.

The Reverse Book Building (RBB) Method

Imagine an auction, but in reverse. Instead of buyers bidding up the price, it’s the shareholders—the sellers—who state the price at which they’re willing to part with their shares. That's the core idea behind the Reverse Book Building, or RBB, process.

Here’s how it works. The company announces the floor price and then opens a bidding window. During this time, shareholders tender their shares, each indicating the minimum price they’d accept.

Shareholders can place their bids at any price they want, as long as it's above the floor price.

After the bidding window slams shut, the company gets to work, sorting through all the bids.

The final discovered price (or exit price) is the price point where the company gathers enough shares to hit that critical 90% shareholding mark.

Now, what if the price discovered is just too steep for the promoter? They do have one move left: a counter-offer. But they can only play this card if they've received tenders from at least 50% of the public shareholders, among other conditions.

The Fixed Price Method

While the RBB method is democratic, it can also create a lot of uncertainty and sometimes even fuel speculation. To provide a simpler alternative, SEBI brought back the Fixed Price method. This was a major recent update to the delisting rules, specifically designed to address concerns about the wild price swings sometimes seen with RBB and to create a more predictable outcome. You can find an excellent analysis of SEBI's balanced approach with this method.

With this approach, things are much more direct. The company makes a straightforward, take-it-or-leave-it offer. There's no bidding, no discovery, no fuss. The promoter simply announces one fixed price at which they’re prepared to buy back all the shares.

Under the current SEBI delisting regulations, this fixed price can't be just any number. It must include a premium of at least 15% over the calculated floor price. This built-in premium guarantees that the offer is already a step up from the baseline valuation. From there, shareholders simply decide whether to accept the price and tender their shares. It’s a clean, upfront mechanism that gives both the company and its investors certainty from day one.

Choosing between the democratic, but unpredictable, RBB and the straightforward Fixed Price method involves a big strategic trade-off. Let's break down the key differences.

Reverse Book Building vs Fixed Price Delisting

Feature

Reverse Book Building (RBB)

Fixed Price Method

Price Determination

Price is "discovered" by shareholders through a bidding process.

Price is pre-determined and offered by the promoter.

Shareholder Role

Active. Shareholders collectively determine the final exit price.

Passive. Shareholders can only accept or reject the offered price.

Price Certainty

Low. The final price is unknown until the bidding process ends.

High. The price is known from the very beginning.

Mandatory Premium

No mandatory premium over the floor price, but the discovered price is often higher.

A minimum premium of 15% over the floor price is required.

Potential Outcome

Can result in a very high exit price if shareholders hold out for a better deal.

Provides a guaranteed premium, but with no potential for a higher "discovered" price.

Process Complexity

More complex and longer, involving a bidding period and price discovery.

Simpler and faster, with a direct offer and acceptance period.

Ultimately, the choice of method says a lot about the promoter's strategy—whether they prefer to negotiate with the market or make a clean, decisive offer. For shareholders, understanding these two paths is crucial to making an informed decision when a delisting offer comes along.

What Are My Rights as an Investor?

When a company you've invested in decides to delist, it's easy to feel like you, the small shareholder, are being pushed around by the big promoters. But that’s not the full picture. The SEBI delisting regulations were created for this very reason: to make sure you have a real say in the matter.

Think of these rules less as procedural red tape and more as your personal toolkit for protection. They give you, the minority shareholder, a powerful voice and ensure you aren't just a bystander in the process. Knowing your rights here is the best way to make sure you get a fair deal.

Your Power at the Ballot Box

The first and most direct power you have is your vote. A company can't just decide to delist with a simple "yes" from a majority of all shareholders. SEBI has put a much higher, and frankly brilliant, hurdle in place specifically to empower public investors like you.

Let that sink in. This isn't just about the promoters getting their way. It completely changes the dynamic. A unified group of public shareholders, even a minority, can stop a delisting in its tracks if they believe the offer isn't fair. Your vote isn't a suggestion; it's a potential veto.

The 90% Hurdle: A Crucial Safeguard

Even if the vote passes, the delisting is far from a sure thing. The next major protection is what’s known as the 90% threshold. For the delisting offer to succeed, the promoter must end up with at least 90% of the company’s total shares after buying out public shareholders.

So, what does this actually mean for you?

You Have Collective Bargaining Power: If a large number of public shareholders hold out because the price is too low, the promoter simply can't reach that 90% target.

The Offer Can Fail: If the 90% mark isn't met, the whole delisting offer collapses. Any shares you tendered are returned to you, and the company stays listed on the stock exchange.

It Forces a Fairer Price: This rule essentially compels promoters to propose a price that is attractive enough to win over the vast majority of public investors.

Don't Worry, You Get a Second Chance

What if you missed the initial offer window? Or maybe you decided to hold onto your shares, only to change your mind later? SEBI has thought of that, too.

Even after a delisting is successful, the promoter is legally required to keep the offer open and accept shares at the final delisting price for at least one year from the date of delisting. This acts as a vital safety net, giving you plenty of time to reconsider and sell your shares.

Of course, after this one-year period, your shares officially become unlisted, which comes with its own tax considerations. If you want to dive deeper into that, our guide on the capital gain on unlisted shares is a great resource. This extended exit right ensures you aren't left holding illiquid shares just because you didn't act immediately.

Common Questions About SEBI Delisting Regulations

undefined

Navigating the world of corporate actions can bring up a lot of practical questions. When a company announces it’s going private, it’s completely natural to feel uncertain about what happens next. To cut through the confusion, we’ve put together answers to some of the most common questions investors have about SEBI delisting regulations.

Our goal is to give you direct, clear-cut answers to these pressing concerns. Getting a handle on these scenarios will help you make smarter, more confident decisions if you ever find yourself holding shares in a company on its way off the stock exchange.

What Happens if I Don't Participate in the Delisting Offer?

This is probably the biggest worry for most investors. If a voluntary delisting goes through and you decide not to sell your shares, you don’t lose them. You’re still the legal owner, but what you own changes dramatically—your shares become unlisted.

The immediate consequence? A massive drop in liquidity. You can’t just log into your trading account and sell them anymore. Finding a buyer becomes a private, off-market task, which is often a complicated and drawn-out process.

This one-year window is your second chance to exit at the same fair price everyone else got. But once that year is up, your options narrow considerably. You’d have to find a private buyer on your own, likely at a much lower price, which is why understanding the clock is ticking is so important.

Can a Company Be Forced to Delist?

Yes, absolutely. A company can be kicked off a stock exchange in what’s known as a compulsory delisting. This isn’t a strategic choice by the company but a penalty imposed by the stock exchange or SEBI for serious misconduct.

Compulsory delisting is the final step after a company has repeatedly broken the rules. Think of it as a corporate red card. Common triggers include:

Failing to pay annual listing fees for a long time.

Persistent violations of corporate governance standards.

Having its shares suspended from trading for an extended period, typically more than six months.

Why Is the 90 Percent Shareholding Threshold So Important?

The 90% threshold is arguably the most powerful tool minority shareholders have under the SEBI delisting regulations. For any voluntary delisting to succeed, the promoter's stake, combined with all the shares tendered by the public, must hit at least 90% of the company's total shares.

If this critical mass isn't reached, the whole delisting offer fails. Simple as that. All the shares tendered by investors are returned to their Demat accounts, and the company stays listed.

This rule essentially gives public shareholders a collective veto. It prevents a promoter from strong-arming a delisting at a low-ball price. To succeed, they have to make an offer that is genuinely attractive enough to convince an overwhelming majority of shareholders to sell.

How Is the Floor Price for a Delisting Offer Calculated?

The floor price is the absolute minimum price a promoter must offer shareholders in a voluntary delisting. It’s not a random number; SEBI has a specific formula to ensure it’s grounded in recent market reality and provides a fair starting point.

The floor price is set as the higher of these two calculations:

The volume-weighted average price (VWAP) of the shares over the 26 weeks leading up to the public announcement.

The VWAP of the shares over the two weeks leading up to the public announcement.

At Unlisted Shares India, we are committed to empowering investors with the knowledge and tools needed to navigate both public and private markets. Whether you're exploring pre-IPO opportunities or managing a diverse portfolio, our platform provides the clarity and access you need. Discover a world of investment possibilities with our expert insights and secure marketplace. Explore your options today at Unlisted Shares India.

Share:

Our Blogs

Our blog provides insightful information about unlisted shares, offering a deeper understanding of how these assets work, their potential benefits, and the risks involved. Whether you're new to unlisted shares or looking to expand your knowledge, we cover topics such as investment strategies, valuation methods, market trends, and regulatory aspects. Stay updated with expert tips and guides to navigate the unlisted share market effectively.