LTCG on Unlisted Shares: Maximize Your Returns Today

7 May 2025

14 min read

Decoding LTCG on Unlisted Shares: The Essentials

Unlisted shares present a unique investment avenue within the Indian financial market. Understanding the tax implications, particularly Long Term Capital Gains (LTCG), is essential for optimizing your investment returns. This section provides a breakdown of the key aspects of LTCG on unlisted shares, guiding you through this distinct asset class.

Understanding the Basics of Unlisted Shares and LTCG

Unlike listed shares that are traded publicly on stock exchanges, unlisted shares are held privately. This fundamental difference significantly affects their taxation. For more information on unlisted shares, see Unlisted shares meaning. A specific holding period must be met for gains to be considered long-term, impacting the applicable tax rate.

The 24-Month Holding Period: A Defining Factor

The holding period for LTCG on unlisted shares is critical for investors. Holding shares for more than 24 months (2 years) qualifies gains as long-term. This duration has substantial implications for your tax liability. Holding shares for less than 24 months results in gains being taxed at your individual slab rate, potentially much higher than the LTCG rate.

Recent Policy Changes: Reshaping the LTCG Landscape

India's taxation framework treats LTCG on unlisted shares differently than listed shares, both in terms of the applicable tax rate and the holding period. Unlisted shares must be held for more than 24 months to qualify for LTCG. As of the July 23, 2024 amendment, LTCG on unlisted shares is taxed at a flat rate of 12.5% without indexation benefits. Indexation previously adjusted the purchase price for inflation, reducing the taxable gain.

This change represents a significant policy shift. Before this amendment, LTCG from unlisted shares was taxed at 20% with indexation. For example, if the capital gain from selling unlisted shares is ₹10 lakhs, the tax at 12.5% is ₹1.25 lakhs. Under the previous 20% rate with indexation on a smaller base (e.g., ₹8 lakhs), the tax would have been ₹1.6 lakhs.

This adjustment reduces the tax burden for long-term investors in unlisted shares, making longer holding periods more appealing. It also simplifies tax calculations by eliminating indexation complexities. The 24-month threshold emphasizes the importance of carefully planning your exit strategy to benefit from the lower LTCG rate. Short-term capital gains (less than 24 months) are taxed at the individual's slab rate, which can be significantly higher. Learn more about taxation on unlisted shares.

The shift from 20% with indexation to a flat 12.5% has significantly altered investor approaches, encouraging longer-term holding and simplifying calculations. This change presents potential advantages for those willing to hold their investments.

The New Reality: LTCG Tax Rates That Change Everything

The Indian landscape for Long-Term Capital Gains (LTCG) on unlisted shares has shifted significantly. Moving from a 20% rate with indexation to a flat 12.5% rate has altered investment strategies. This necessitates a closer examination of how these changes influence potential returns.

Impact on Holding Periods and Returns

The previous indexation benefit provided inflation relief for longer holding periods. The new flat rate changes this dynamic. Consider a five-year investment compared to a three-year investment. Under the old regime, indexation would have substantially reduced the five-year investment's taxable gain. Now, the 12.5% rate applies equally, lessening the holding period's tax-related importance. Investors may now favor shorter holding periods for unlisted shares.

High-Growth vs. Stable Investments: A New Perspective

Indexation removal affects different unlisted shares differently. High-growth investments, expected to appreciate significantly, previously benefited greatly from indexation, mitigating the tax burden. The flat rate increases the absolute tax on these investments. The impact is less dramatic on stable, lower-growth investments.

Who Benefits Most From the New 12.5% Regime?

The new regime benefits certain investors. Those seeking medium-term gains in unlisted shares might find the 12.5% rate more appealing than the previous 20%, even without indexation. This simplifies calculations and potentially boosts returns for shorter-term holdings. Lower tax bracket investors also benefit proportionally more from the reduced rate.

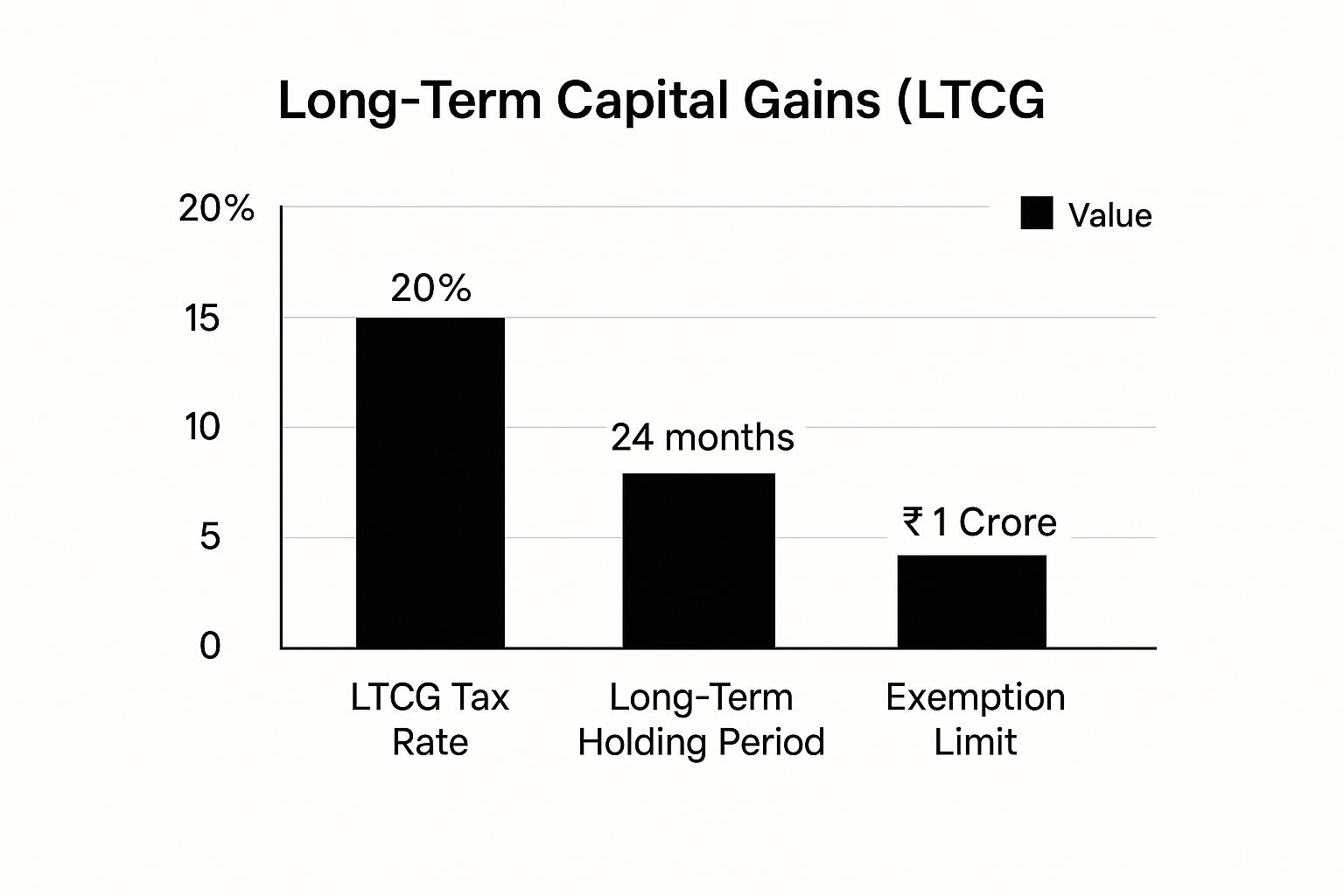

Visualizing the Key Changes

The following infographic illustrates the main changes: a shift from 20% with indexation to a flat 12.5%, retaining the 24-month holding period for LTCG and the ₹1 Crore exemption limit.

This infographic highlights the rate reduction, potentially encouraging unlisted share investment while emphasizing the continued importance of the 24-month holding period for LTCG qualification. This simplification benefits investors through easier tax planning.

To better understand the practical implications of these changes, let's analyze the impact on different investment scenarios using a comparison table.

The table below, "LTCG Tax Rates on Unlisted Shares: Before and After," compares the previous and current regimes, highlighting their impact on investors.

Parameter

Previous Regime

Current Regime

Impact on Investors

Tax Rate

20% with Indexation

12.5% (Flat)

Simpler calculation, potentially lower tax burden for shorter-term holdings, higher tax burden for long-term, high-growth investments without indexation benefit.

Holding Period for LTCG

24 months

24 months

No change; maintains the long-term investment horizon.

Exemption Limit

₹1 Crore

₹1 Crore

No change; maintains the exemption threshold for larger gains.

Indexation Benefit

Applicable

Not Applicable

Loss of inflation protection for longer-term investments.

This comparison underscores the trade-offs between the old and new regimes. While the lower rate is attractive, the absence of indexation necessitates careful consideration, especially for high-growth, long-term investments.

Analyzing Real Portfolio Examples

Let’s examine some practical scenarios:

Startup Investments: A five-year, high-growth startup investment would have previously benefited from indexation. Now, the flat 12.5% applies to the total gain.

Private Equity Holdings: The impact is similar for long-term private equity. While 12.5% is lower than 20%, the lack of indexation can increase the tax burden on substantial appreciation.

Traditional Unlisted Securities: For stable unlisted securities with moderate growth, the new regime may be more favorable.

NRI Investors: Navigating LTCG on Unlisted Shares

Investing in India's unlisted shares market offers unique opportunities for Non-Resident Indians (NRIs). However, recent adjustments to the Long-Term Capital Gains (LTCG) tax laws require careful review. This section explains how these changes affect NRIs and offers insights for optimizing after-tax returns.

Understanding the Shift in LTCG Tax Rates

Previously, NRIs benefited from a 10% LTCG tax rate on unlisted shares. This rate has been increased to 12.5%, bringing it in line with the rate for resident taxpayers. While a 2.5% increase may seem minor, it represents a 25% increase in the actual tax burden. This significantly impacts the investment landscape for NRIs.

This change eliminates the preferential tax treatment previously enjoyed by NRIs. As a result, NRIs now need to re-evaluate their investment strategies to ensure they continue to achieve optimal returns.

Case Studies: Illustrating the Impact

Consider an NRI who invested ₹2,00,000 (approximately USD 4,000 at an exchange rate of ₹50/USD) in 10,000 unlisted shares at ₹20 per share. Under the previous 10% tax rate, any profits exceeding the initial investment would be taxed at that lower rate. With the new 12.5% rate, the tax liability on those same gains is now higher. This difference becomes even more significant as the investment value grows.

Investment Structures and Currency Fluctuations

The increased LTCG tax rate encourages NRIs to explore tax-efficient investment structures. Holding unlisted shares through certain entities may offer potential tax advantages. Additionally, fluctuating exchange rates between the Indian Rupee and foreign currencies have a greater impact on overall returns. NRIs should carefully consider these fluctuations when evaluating potential profits and calculating their tax liabilities.

Documentation and Compliance

Maintaining accurate documentation is crucial for complying with the revised LTCG rules. Keeping detailed records of purchase dates, prices, and sale transactions is essential for accurately calculating capital gains and meeting tax obligations. This meticulous record-keeping is particularly important for NRIs due to the added complexities of international transactions and currency conversions.

Comparing Investment Avenues

NRIs should compare the revised LTCG tax on unlisted shares with other investment opportunities available in India. Evaluating the after-tax returns from various investment avenues, such as fixed deposits, mutual funds, and listed shares, will help determine the most suitable investment strategy. This comparative analysis allows NRIs to optimize their portfolios for the best possible returns.

Restructuring Existing Portfolios

NRIs with existing investments in unlisted shares might need to restructure their portfolios to adapt to the new tax landscape. This could involve rebalancing their holdings, exploring different exit strategies, or considering alternative investment avenues. A thorough review of existing portfolios in light of the revised tax laws can help maximize after-tax returns. This proactive approach is crucial for navigating the new tax regime and optimizing investment outcomes. More detailed information on these changes can be found here.

Master the Math: Calculating LTCG on Unlisted Shares

undefined

This section offers practical guidance on accurately calculating Long-Term Capital Gains (LTCG) on unlisted shares. Understanding this process is essential for both regulatory compliance and maximizing your investment returns.

Determining Acquisition Cost and Sale Consideration

The first step is accurately documenting your acquisition cost. This includes the original purchase price, brokerage fees, stamp duty, and any other related expenses. For inherited shares, the acquisition cost is usually the fair market value at the time of inheritance. Similarly, for shares received through an Employee Stock Ownership Plan (ESOP), the cost basis depends on the exercise price and any taxes paid upon conversion. You might be interested in: How to calculate the fair value of unlisted shares.

The next step is verifying the sale consideration. This is the total amount received from selling the shares, less any transaction costs like brokerage fees and Securities Transaction Tax (STT). Accurate documentation of these figures is vital for determining the net capital gain, forming the basis for all following calculations.

Handling Complex Scenarios

Unlisted share investments can present complex situations that impact LTCG calculations. Bonus share issuances or rights offers affect the per-share cost. For instance, if you initially held 100 shares and received 10 bonus shares, your cost basis is now distributed across 110 shares. This adjustment is essential for accurately calculating the capital gain when selling.

Partial exits, where you sell only some of your holdings, require calculating the gain on the specific shares sold. Proper accounting for these scenarios ensures precise tax calculation. For Non-Resident Indian (NRI) investors, understanding the tax implications is especially important. Read more about the tax implications of Overseas Share Investments.

Valuation and Documentation: Protecting Your Position

Valuing unlisted shares can be challenging due to the lack of a readily available market price. Different valuation approaches exist, depending on how you acquired the shares (purchase, gift, inheritance, ESOPs, etc.). Meticulous documentation of the chosen valuation method and supporting evidence is crucial for justifying the calculated LTCG during tax assessments. This protects you against potential disputes.

Maintaining detailed records of all transactions, including purchase agreements, sale receipts, valuation reports, and related correspondence, is vital. This thorough documentation provides a strong defense during tax scrutiny.

Practical Examples: Putting Theory Into Practice

The following table provides examples of LTCG calculations in different unlisted share investment scenarios.

This table summarizes how various factors, such as brokerage fees and partial sales, can influence the final LTCG calculation and subsequent tax liability. Understanding these nuances is crucial for effective tax planning.

Strategic Tax Planning for LTCG on Unlisted Shares

Smart investors understand the importance of proactive tax planning. This is especially true when dealing with long-term capital gains (LTCG) on unlisted shares. This section explores legitimate strategies to optimize your tax position and potentially improve your overall investment returns. You might find this article helpful: The benefits of investing in unlisted shares.

Timing Acquisitions and Disposals

The timing of your buy and sell transactions plays a critical role in managing your LTCG tax liability. Holding unlisted shares for more than 24 months qualifies you for a lower LTCG tax rate of 12.5%.

If you anticipate significant price appreciation, holding your shares slightly longer to reach this 24-month threshold can significantly reduce your tax burden. Conversely, if a market downturn seems likely, selling before the 24-month mark and paying a higher short-term capital gains tax rate might be preferable to minimize potential losses.

Entity Structuring for Tax Efficiency

Holding unlisted shares through specific entities, such as a Limited Liability Partnership (LLP) or a family trust, can offer potential tax advantages. These structures offer flexibility in managing income and expenses, possibly lowering your overall tax exposure.

However, the best structure depends on individual circumstances and current regulations. Consulting with a qualified tax advisor is highly recommended. They can help you determine the most suitable approach for your specific situation.

Exit Strategies: Maximizing After-Tax Returns

Different exit strategies can significantly impact your LTCG tax. For startup or private equity investments, a phased exit, where you sell your holdings in stages over time, can distribute your capital gains and potentially lower your overall tax bill.

Share swaps, where you exchange your unlisted shares for shares in a listed company, can defer capital gains tax until you sell the listed shares. Reorganizations, like mergers or acquisitions, can also present tax-efficient exit opportunities.

Documentation: Your First Line of Defense

Meticulous documentation is essential. Maintain records of all purchase and sale agreements, valuation reports, and any other relevant documents. This thorough documentation substantiates your LTCG calculations during tax assessments.

Detailed records not only strengthen your position during audits but also help prevent disputes with tax authorities. Documenting the rationale behind your investment decisions, including timing and entity structure, can further support your tax strategy.

Integrating Unlisted Shares into Your Portfolio

Strategically integrating unlisted shares into your overall investment portfolio can improve overall tax efficiency. Balancing your portfolio across different asset classes with varying tax treatments can help optimize your total tax liability.

For instance, offsetting gains from unlisted shares with losses from other investments can reduce your net taxable income. Remember to prioritize your investment objectives and risk tolerance while considering tax implications. A balanced approach ensures your investment strategy aligns with your financial goals while maximizing after-tax returns.

Reality Check: LTCG Myths That Cost Investors Money

Navigating the complexities of Long-Term Capital Gains (LTCG) on unlisted shares can be tricky. Several misconceptions often lead to costly mistakes and missed opportunities for investors in India. This section aims to debunk some of these common myths, offering clarity and helpful guidance.

Myth 1: Valuation Is Always Straightforward

A frequent misunderstanding centers around how unlisted securities are valued. Unlike listed shares with a publicly traded market price, unlisted shares require a more nuanced approach. Some investors mistakenly assume they can assign any value. However, tax authorities carefully examine valuation methods during assessments. Strategic tax planning often involves understanding the complexities of tax valuation to optimize LTCG results.

Different valuation methods are appropriate for various acquisition scenarios, such as purchases, gifts, inheritance, or Employee Stock Ownership Plans (ESOPs). Maintaining proper documentation of the chosen method and providing supporting evidence is critical for justifying the declared value.

Myth 2: The 24-Month Holding Period Is Simple

The 24-month holding period rule, while seemingly straightforward, can be complicated by specific events like bonus share issuances, rights offers, and mergers. Investors sometimes misinterpret how these events impact the holding period of their shares. Bonus shares, for instance, usually inherit the holding period of the original shares. Shares acquired through rights issues, however, have a new holding period beginning on the allotment date.

Keeping accurate records of these adjustments is crucial for correctly classifying gains as long-term or short-term. Misclassifying gains can result in unexpected tax liabilities.

Myth 3: Documentation Isn’t That Important

Many investors undervalue the importance of thorough documentation, believing that knowing the purchase and sale prices is enough. However, detailed records of the entire transaction are essential. This includes purchase agreements, sale receipts, valuation reports, and any supporting evidence for the chosen valuation method. This documentation is vital for protecting your position during tax assessments.

Comprehensive documentation substantiates your calculations and strengthens your case during scrutiny by tax authorities. This helps prevent disputes and ensures compliance with tax regulations.

Myth 4: Listed and Unlisted Shares Are Treated the Same

A significant misunderstanding arises from assuming listed and unlisted shares are treated identically for tax purposes. They are subject to different tax rates and rules. For example, while both are now taxed at a flat 12.5%, other distinctions remain, particularly concerning valuation and documentation.

Overlooking these differences can lead to incorrect tax calculations and potential penalties. It’s important to understand the specific rules applicable to each share type.

Myth 5: Inherited and Gifted Shares Don’t Have LTCG Implications

Inherited and gifted shares also require careful attention. The holding period and cost basis for these shares differ from purchased shares. The holding period for inherited shares begins on the original holder's date of death. The cost basis is typically the fair market value at the time of inheritance. For gifted shares, both the holding period and cost basis transfer from the giver.

Failing to consider these unique circumstances can lead to substantial miscalculations of LTCG.

Case Study: Costly Misclassification

Consider an investor who purchased unlisted shares in 2022 and received bonus shares in 2023. They then sold all shares in 2025, assuming the entire holding period exceeded 24 months. However, the bonus shares have a separate holding period from their issue date. Misclassifying the gains from these bonus shares as LTCG could result in an inaccurate tax calculation and potential penalties.

Understanding these nuances is crucial for accurate LTCG calculations and informed investment decisions. Addressing these myths proactively ensures compliance and maximizes investment returns.

Our blog provides insightful information about unlisted shares, offering a deeper understanding of how these assets work, their potential benefits, and the risks involved. Whether you're new to unlisted shares or looking to expand your knowledge, we cover topics such as investment strategies, valuation methods, market trends, and regulatory aspects. Stay updated with expert tips and guides to navigate the unlisted share market effectively.