What Is an Illiquid Stock? Complete Guide With Examples

Illiquid Stocks Meaning Explained

Illiquid stocks are securities that cannot be readily bought and sold in the market with much influence on its price or take a lot of time to make a purchase. Very opposite of the term liquid is the term illiquid, which describes assets which cannot be turned into cash easily within a short period without significant impairment. These stocks can be described as having a small trading face, fewer players in the market and can hardly find willing buyers or sellers at any particular time.

The very nature of illiquidity is based on the imbalances of supply and demand in the stock market. In case of a lack of buyers and sellers actively trading on a specific stock, it is hard to conduct transactions efficiently. This fact leads to a market environment in which even small trades can lead to very large price changes and thus these stocks are naturally more volatile and risky to investors. To address this issue, the Securities and Exchange Board of India (SEBI) and other regulatory authorities have adopted special trading arrangements like periodic call auctions of stocks whose liquidity is below some specified liquidity-related thresholds.

What Is an Illiquid Stock With Examples

The stock of smaller companies, specialty businesses or companies in niche markets that have little investor attention are normally considered as being illiquid. These stocks are usually small-cap and micro-cap stocks with a market capitalization of less than 5,000 crores in the Indian market.

Illiquid nature is common in real estate businesses, specialty manufacturing companies and those in weakening industries. As an example, companies that are engaged in conventional manufacturing, some commodity firms, or those that have issues with regulation often witness decreased amounts of trading, thus, their stocks become illiquid. The same applies to private company shares, untraded securities and shares in companies experiencing financial distresses, as they can have restricted buyer interest and are not readily transferable.

The Bombay Stock Exchange (BSE) in the Indian stock market has lists of illiquid securities that are revised quarterly. These listings contain stocks which do not qualify by trading minimum volume and are then transferred to periodic call auction systems instead of continuous trading periods. The stocks of companies in declining industries, businesses with less institutional coverage, or with concentrated ownership tend to become illiquid as a result of less market presence.

International exceptions are penny stocks, stock of bankrupt companies and stocks of companies at risk of being delisted. Illiquid properties are also common in stocks of firms with extremely high share prices (so that may be less accessible to retail shareholders), those with low free float (because of promoter ownership), and securities of firms in highly specialized or falling industries.

Key Features of Illiquid Stocks

The main feature of illiquid stocks is a dramatically low trading volume which averages low levels, less than 100,000 shares in a day. This small volume implies that there is low interest of investors and limited participation of investors in the market hence investors find it hard to sell or buy large volumes of stocks without influencing the price of the stock. The volume of trading can also be so small that there are days or weeks where no one trades in any stock, which makes liquidity even more difficult.

Another characteristic of illiquid stocks is the wide bid-ask spreads. Bid-ask (the difference between the maximum price buyers are willing to pay and the minimum price sellers are willing to accept) varies by a substantial amount on illiquid stocks than on liquid stocks. Whereas liquid stocks may have a spread of 0.1-0.5, an illiquid stock may have a spread of 5-10 percent and sometimes even greater, significantly increasing the transaction cost incurred by affected investors.

Another important characteristic of illiquid stocks is a lack of institutional interest. Institutional investors, such as mutual funds, pension funds and insurance companies, generally sell illiquid stocks because they are large and easily get changed into a portfolio. This lack of institutional participation further pulls down the trading volumes and interest in the market producing a self-perpetuating force of illiquidity.

Risks of Investing in Illiquid Stocks

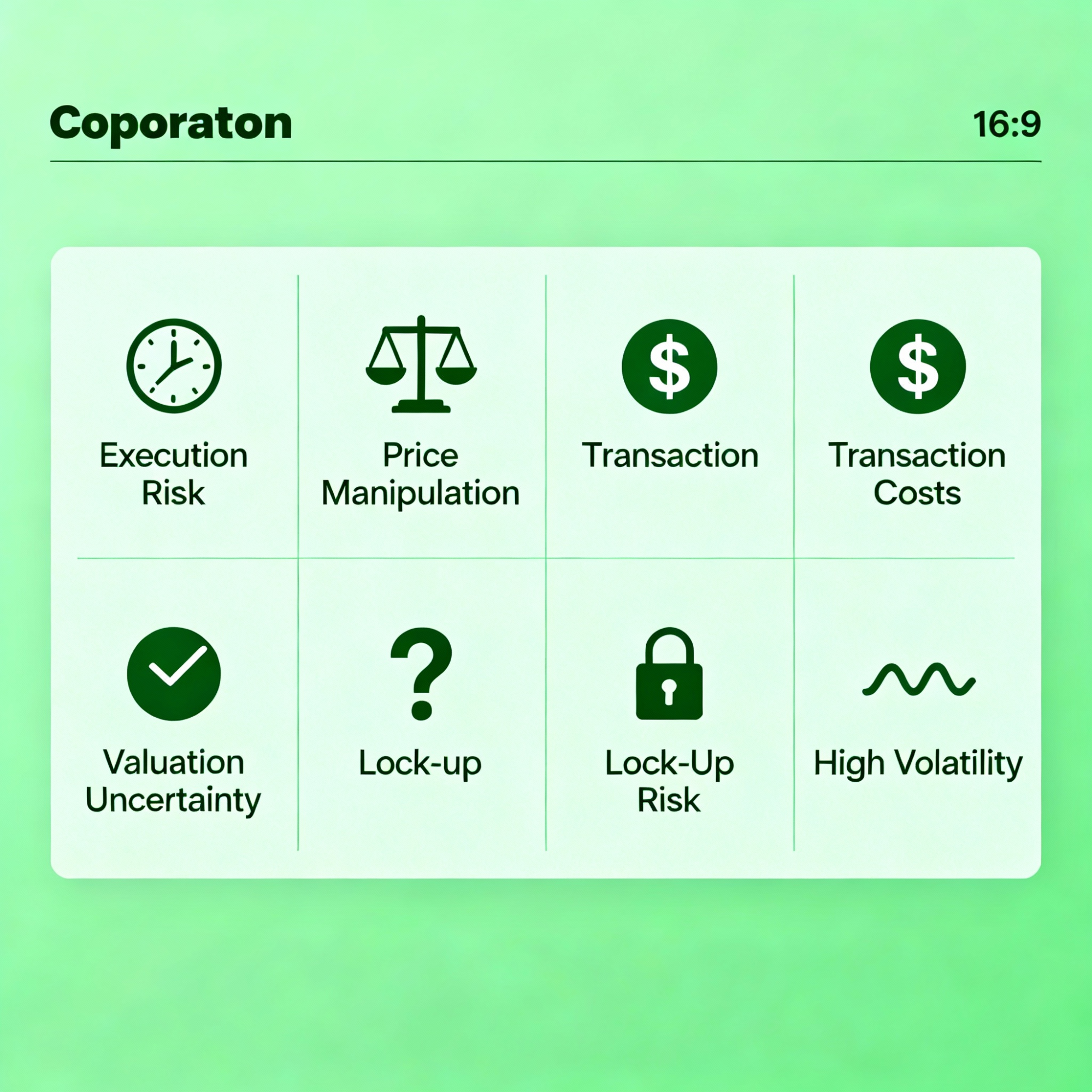

The most direct problem with the investment in illiquid stocks is execution risk. It could be very hard since an investor would not be able to sell or purchase shares at the preferred prices and this may lead to postponed transactions or having to accept the available prices which are not favorable. Illiquid stocks can sometimes be virtually unsaleable at a large discount to their perceived value when there is market stress or investors are forced to exhaust positions in a short period of time.

The illiquids have high risks of price manipulation since they trade in low volumes. Groups of people who invest in stock or even single traders can potentially manipulate the price of stocks by undertaking organized buying or selling actions in order to cause artificial price changes that may not be indicative of the underlying company fundamentals. This manipulation risk is especially high in penny stocks and very small-cap companies that have very low capital requirements to significantly manipulate the prices.

Illiquid stock investing is risky as a result of transaction costs. The huge spreads of these securities imply that investors incur losses as soon as they buy them, because they have to pay the high ask price and can only sell them at the low bid price. These high transaction costs may considerably reduce the returns to investment especially to those investors who will be required to execute frequent trades or to change their position.

The other risk factor that is critical to illiquid stocks is valuation uncertainty. Trade in such securities is also less frequent such that it becomes difficult to establish the correct values of such securities in the market. It also follows that since there are no regular price discovery mechanisms, the quoted prices do not necessarily indicate the actual market values, hence resulting in huge losses in trying to liquidate the positions later.

Capital lock-up risks are substantial with illiquid stocks, as investors may find their capital tied up for extended periods without the ability to access funds when needed. This illiquidity can prevent investors from taking advantage of other investment opportunities or meeting unexpected financial obligations. During market downturns, this risk becomes particularly acute as liquidity typically decreases further, potentially trapping investors in losing positions.

Liquid Stocks vs Illiquid Stocks

The basic distinction between liquid and illiquid stocks is the ease of trading them and the effect of the transactions on the market price. Liquid stocks have the advantage of large trading volumes, large number of market players, and the capacity of conducting large transactions without causing significant prices of stocks. Contrastingly, illiquid stocks are afflicted with low trading volumes, low market participation and even minor trades can result in large price changes.Trading efficiency varies widely between liquid and illiquid stocks.

Liquid stocks enable the buyer and sellers of stocks to enter and exit rapidly and at fair market prices, which offers the portfolio management and risk control flexibility. The large transactions can be completed by investors at minimal price impacts and this makes these stocks appropriate to institutional investors and active trading strategies.

There is a wide difference in the risk-return profiles of liquid and illiquid stocks. Although liquid stocks typically have smaller returns because they are highly efficient and have a large number of analysts, they have more predictability and reduced transaction costs. Inefficiently priced and under-covered by analysts, illiquid stocks can have superior potential returns, but with significantly greater risks and costs.

How to Identify Illiquid Stocks in the Market

The trading volume analysis is the most common way of identifying illiquid stocks. Investors ought to look into average trading volumes in terms of total shares outstanding, of which stocks trade less than 100,000 shares in any one day or whose average volumes are much lower than those of their sector. Irregular trading patterns of the stocks, including days where no trading was done, are clear indications of illiquidity problems.

Another good predictor of stock illiquidity is the bid-ask spread analysis. The spread as a percentage of the price of the stock can be calculated by investors who divide the price of the ask and bids by the prevailing price of the stock. Spreads over 2-3 percent are always indicative of illiquid states, whereas spreads over 5 percent are indicative of extreme illiquidity which can result in trading which is prohibitively costly.

The market capitalization analysis is used to determine potentially illiquid stocks since smaller firms with market caps less than 1,000 crores in the market are usually faced with liquidity issues. Nevertheless, market capital is not an adequate criterion, as certain large firms can experience temporary liquidity crises under certain conditions or in a given situation in the market.

The exchange-specific indicators may assist investors to recognize the illiquid stocks based on the official listing and classifications. The BSE issues quarterly lists of illiquid securities which are transferred into periodic call auction mechanisms and gives a direct point of reference to investors who wish to avoid or target illiquid stocks in particular. On the same note, shares that are not members of key indices such as the Nifty 50 or Sensex are prone to be illiquid, but not always.

The other tool of identification is institutional ownership levels, because the stocks with low institutional ownership tend not to have the trading liquidity that the institutions introduce in the market. The firms that are less than 10% institutional ownership or the firms that do not exist in the institutional portfolios can be challenged by liquidity issues. Also, the stocks of the industries that are in decline or those with low levels of analyst coverage often become illiquid because of lower levels of investment interest.

Price and volume trends can be technical indicators that can identify illiquid stock characteristics. Stocks that experience long spells of sideways trading and then sharply change in price, coupled with irregular surges of volume ordinarily signify illiquidity. Even chart patterns that indicate a gap between trading sessions or days that have no price changes are also indicative of liquidity problems.

Conclusion

The risk-return trade-off inherent in illiquid stocks requires investors to carefully assess their risk tolerance, investment objectives, and liquidity needs before committing capital to these securities. While experienced investors may find opportunities in undervalued illiquid stocks, the majority of market participants benefit from focusing on liquid securities that offer greater flexibility, lower transaction costs, and more predictable execution. As markets continue evolving, the distinction between liquid and illiquid stocks remains fundamental to successful investment strategy and portfolio management.